- The Comptroller and Auditor General (CAG) of India is an authority, established by the Constitution of India under article 148.

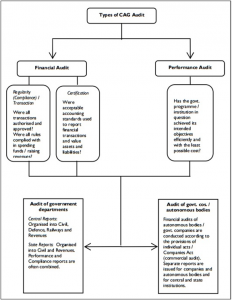

- CAG audits all receipts and expenditure of the Government of India and the state governments, including those of bodies and authorities substantially financed by the government.

- The CAG is also the external auditor of Government-owned corporations and conducts supplementary audit of government companies, i.e., any non-banking/ non-insurance company in which the state and Union governments have an equity share of at least 51% or subsidiary companies of existing government companies.

- The reports of the CAG are taken into consideration by the Public Accounts Committees (PACs) and Committees on Public Undertakings (COPUs), which are special committees in the Parliament of India and the state legislatures.

- The CAG enjoys the same status as a judge of Supreme Court of India in Indian order of precedence.

- Appointment: CAG is appointed by the President of India following a recommendation by the Prime Minister. On appointment, he/she has to make an oath or affirmation before the President of India.

- Removal: The CAG can be removed only on an address from both house of parliament on the ground of proved misbehaviour or incapacity.The CAG vacates the office on attaining the age of 65 years age even without completing the 6 years term.

- Demand to make CAG responsible to parliament through constitutional amendment

- Often CAG’s report are not presented to legislature on time, as they might be deemed inconvenient by the government of the day. This dilutes CAG’s effectiveness in ensuring Executives accountability to parliament

The present constitutional structure ensures independence of the CAG to go into the entire gamut of audit functions where public interest is involved.

It is useful to draw the public’s attention to Article 324 of the Constitution, which fully empowers the Election Commission of India (ECI) to superintend, direct and control the election of the President, the Vice-President and the legislatures, both at the Centre and in the States. Apropos the elections, the powers of the ECI are absolute and even litigation before the judiciary can only come after the completion of the election process.

Independence of the CAG

As the chief enforcer of financial accountability of the government, it was imperative for the CAG to remain independent of the political executive and for the Constitution to demonstrate as such. This was guaranteed by provisions protecting the salary, tenure and pensions, prohibition on his removal save by impeachment and a bar on post-retirement employment. Curiously, no analogous protection was devised for the selection criteria and appointments mechanism which would be at the sole discretion of the executive.

Selection of the CAG

Nemo judex in causa sua i.e. no person shall be a judge in his own cause, is a fundamental principle of administrative law that governs conflicts of interest. Though the CAG is not a judge in law, his task of auditing government accounts, as a matter of principle, requires independence from the government analogous to that enjoyed by a judicial officer. Such a principle will unarguably be violated if an officer audits his own Ministry’s actions, irrespective of how upright he himself might be.

Appointment processes

Currently the Comptroller and Auditor General of India is appointed by the President of India following a recommendation by the Prime Minister. The Supreme Court has repeatedly held that the test for determining whether a decision-making authority is perceived to be impartial is whether there is a reasonable apprehension of bias from the point of view of an average honest man. One of the key factors giving rise to such an apprehension is the manner of appointment. Also, High Powered Committee of The National Commission to Review the Working of the Constitution recommended that the power of appointment be kept “outside the exclusive power of the Executive”. Accountability demands that not only must processes of government be transparent; equally the government must publicly justify its decisions.

Thus, to ensure Independence of the CAG — firstly the appointment of the CAG should be facilitated by a Bipartisan collegium — Also, the list of candidates and criteria adopted must be made public — this will help in removing the “apprehension of bias”

Limitations on CAG

- Unlike the Supreme Court, the CAG’s powers are severely circumscribed by Sections 14, 15, 19(3) and 20(1) of the DPC Act.

- It curtails his overarching power over authorities that are substantially funded by governments (i.e. 51 per cent or more of their annual expenditure).

- Without prior government sanction, the CAG is precluded by rule/law from auditing all other entities, such as PPP partners, private contractors, regulators, NGOs, local quangos (such as municipalities and panchayats).These agencies receive large government funding or their functioning involves the exploitation of both national and natural resources.

- By Section 15(2) of the DPC Act, the CAG can be deprived of his authority to conduct an audit if the organisation is empowered to nominate an agency other than the CAG for the job. And this despite the fact that the government has a large shareholding or interest in its share capital or provides annual budgetary support.

- The CAG unlike SC has no “power to pass any decree, or the investigation or punishment of any contempt of itself on the Supreme Court” — Section 18 of the DPC Act neither provides any deadline for the production of documents and replies to the CAG nor any contempt proceedings for their denial.

- The CAG doesn’t have the right to release these reports in the public domain if they are not presented in the legislature within a month of their submission. Nor can CAG enforce any of its findings by decree, akin to Parliament’s Public Accounts Committee.

- Article 148(5) of the Constitution states that the conditions of service in the Indian Audit and Accounts Department (IA&AD) and the administrative powers of the CAG shall be such as may be prescribed by rules made by the President after consultation with the CAG — however, while the CAG’s budget is not subject to parliamentary vote, the IA&AD has to face regular budget cuts and freeze on recruitment. The CAG is not permitted to recover the IA&AD’s establishment costs from government programmes. Nor does he have the authority to directly hire domain specialists and/or support staff on his own.

- Thus it can be said that the CAG is a prosecutor with a law that hobbles its functioning, a judge without the power to sentence and a litigant with no right of appeal.

Improvements

- The audit mandate does not, for example, cover gram panchayats, which were introduced as a third tier of government under the 73rd Amendment to the Constitution, the emergence of the public-private partnership model or the devolution of funds for schemes such as the rural health mission through bodies such as non-governmental organisations (NGOs).

- A lot of changes require to be incorporated in the Audit Act of 1971 — to address the limitations above.

- Exercise of CAG’s powers in relation to the accounts of the Union and the States is derived from Article 149 of the Indian Constitution. Discuss whether audit of the Government’s policy implementation could amount to overstepping its own (CAG) jurisdiction? (UPSC Mains 2016)

- Distinguish between the auditing and Accounting functions of the CAG of India. (UPSC Mains 2008 )